Risk Management: Alignment of the Plan

Protect What Matters Most

Risk management is the process of identifying, assessing, and minimizing financial risks that could derail your retirement plans. Since retirees no longer have the ability to replace lost income through work, managing risk becomes critical to ensure that your nest egg lasts throughout your retirement years.

Fundamental Aspects of

Risk Management

Market Risk

Definition:

The risk of your investments losing value due to fluctuations in the stock or bond markets.

Management:

- Asset allocation: Shift to a more conservative portfolio as you approach and enter retirement. This means reducing exposure to volatile assets like stocks and increasing investments in bonds, cash, and other stable income-generating assets.

- Diversification: Spread your investments across different asset classes (stocks, bonds, real estate, etc.) to reduce exposure to any single market downturn.

- Bucket strategy: Set aside different "buckets" of money for short-term needs (cash and bonds) and long-term growth (stocks). This helps ensure you're not selling investments at a loss to cover expenses.

Longevity Risk

Definition:

The risk of outliving your savings, which is a growing concern as life expectancy increases.

Management:

- Annuities: Consider purchasing a fixed or immediate annuity to guarantee a lifetime income stream, which can help mitigate the fear of running out of money.

- Conservative withdrawal rates: Follow a sustainable withdrawal strategy, such as the 4% rule, where you withdraw no more than 4% of your retirement savings each year to help ensure your money lasts.

- Delay Social Security: By delaying your Social Security benefits until age 70, you can increase your monthly payment and reduce the risk of outliving other assets.

Healthcare and Long-Term Care Risk

Definition:

The risk of facing high medical costs or needing long-term care, which can quickly deplete savings.

Management:

- Medicare planning: Enroll in Medicare on time and consider supplemental policies (Medigap or Medicare Advantage) to cover gaps in coverage.

- Health Savings Accounts (HSAs): If you had an HSA while working, you can use tax-free withdrawals for medical expenses in retirement.

- Long-term care insurance: Consider purchasing long-term care insurance to protect against the financial impact of needing extended in-home care, assisted living, or nursing home care.

- Self-insurance: If you have substantial assets, you might choose to self-insure for long-term care by setting aside funds specifically for that purpose.

Inflation Risk

Definition:

The risk that rising prices will erode the purchasing power of your savings over time.

Management:

Invest in inflation-protected securities: Consider investing in Treasury Inflation-Protected Securities (TIPS) or other inflation-hedging assets like real estate or dividend-paying stocks.

- Growth investments: Keep a portion of your portfolio in growth-oriented investments, like stocks, to help your savings grow and keep pace with inflation.

- Delay Social Security: Social Security payments are adjusted for inflation, so delaying benefits can provide a higher inflation-protected income later in life.

Interest Rate Risk

Definition:

The risk that changes in interest rates will negatively affect your income, particularly if you rely heavily on fixed-income investments like bonds.

Management:

- Bond laddering: Spread out bond investments across different maturities to minimize the impact of interest rate fluctuations.

- Diversify income sources: Don’t rely solely on bonds for retirement income. Diversify with dividend-paying stocks, real estate, or annuities.

Sequence of Returns Risk

Definition:

The risk of experiencing poor investment returns in the early years of retirement, which can permanently deplete your portfolio if you’re withdrawing money at the same time.

Management:

- Delay withdrawals: If possible, delay withdrawals during market downturns to allow your investments to recover.

- Use a cash buffer: Maintain a cash or short-term bond reserve to cover living expenses during market dips, so you don’t have to sell investments at a loss.

- Dynamic withdrawal strategies: Adjust your spending and withdrawals based on market performance, spending more in good years and less in bad years.

Liquidity Risk

Definition:

The risk of not having enough liquid (easily accessible) funds to cover unexpected expenses or market downturns.

Management:

- Maintain an emergency fund: Keep 6-12 months of living expenses in a highly liquid account (like a savings account or money market fund) to cover unforeseen expenses.

- Avoid over-investing in illiquid assets: Be cautious of tying up too much of your wealth in assets like real estate or private equity, which can be difficult to sell quickly.

Behavioral Risk

Definition:

The risk that emotional decisions (fear, greed, panic) will lead to poor financial choices, such as selling investments during a market crash or overspending.

Management:

- Stay disciplined: Stick to your investment strategy, even when markets get volatile. Avoid making knee-jerk reactions to market drops.

- Use a financial advisor: A financial advisor can provide objective guidance and keep your retirement strategy on track, acting as a buffer against emotional decisions.

Estate and Legacy Risk

Definition:

The risk that your estate won’t be distributed as you intend, or that taxes will reduce the amount left to your heirs.

Management:

- Estate planning: Work with an attorney to create a comprehensive estate plan, including a will, trusts, and clear beneficiary designations.

- Minimize taxes: Use tools like Roth conversions, gifting strategies, and trusts to minimize estate taxes and ensure your heirs inherit as much of your wealth as possible.

Tax Risk

Definition:

The risk of unexpected tax burdens, particularly from required withdrawals from retirement accounts or changing tax laws.

Management:

- Tax-efficient withdrawal strategy: Work with a tax professional to determine the most efficient order for withdrawing from taxable, tax-deferred, and tax-free accounts.

- Roth conversions: Consider converting some of your traditional IRA or 401(k) to a Roth IRA when your tax bracket is lower in early retirement to reduce future taxable income.

Aligning Your Personal Risk Tolerance with Your Situation

and Portfolio

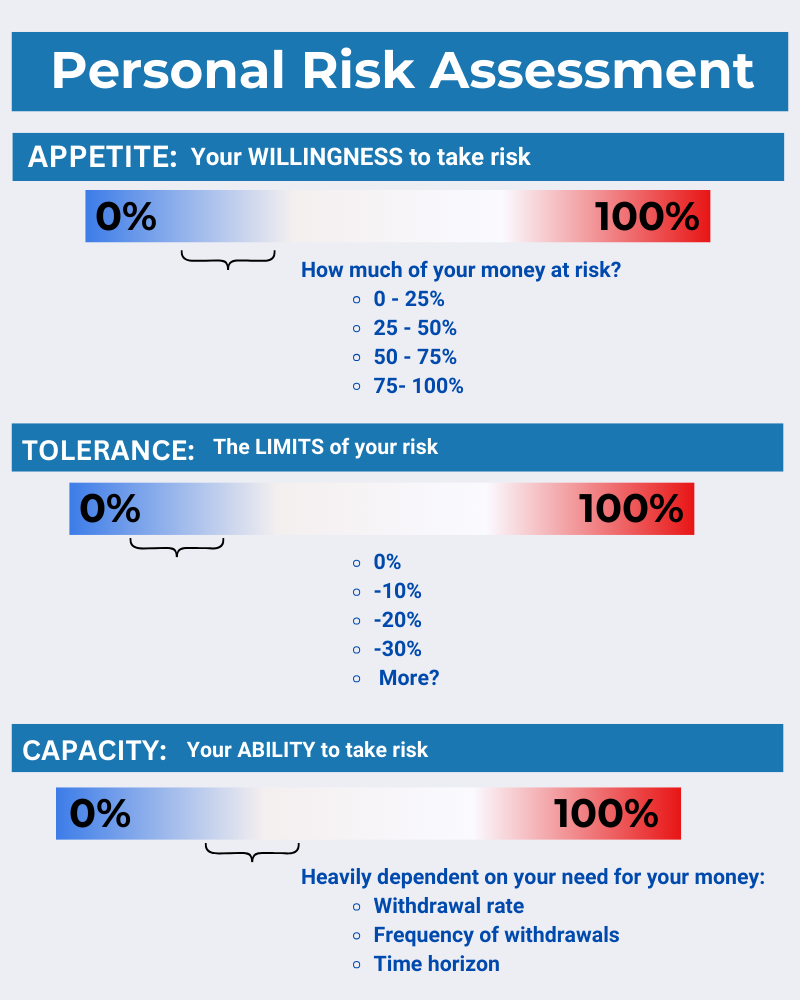

Appetite refers to your willingness to take on risk, which is influenced by how much of your money you are comfortable putting at risk. The image provides different levels of risk exposure: 0%-25%, 25%-50%, 50%-75%, and 75%-100%.

Tolerance represents the limits of your risk capacity, indicating how much loss you can endure. The levels illustrated include potential losses of 0%, -10%, -20%, -30%, and possibly more, depending on your individual situation.

Capacity is your ability to take on risk, which heavily depends on your financial needs. Factors that influence your risk capacity include your withdrawal rate, how frequently you plan to withdraw money, and your investment time horizon.

Safeguard Your Retirement with Proactive Risk Management

In short, risk management for a retiree is all about protecting your savings and income streams from the various financial threats that could throw your retirement off course. It’s a proactive approach to ensure that your money lasts as long as you do, and you don’t face any major financial surprises during your retirement years.

Take the First Step

Toward Financial Security

We help our clients navigate financial markets with confidence while mitigating unnecessary stress and uncertainty.